Investment Methods

Investment Methods of valuation: Generally speaking, an investment is any transaction that is carried out with the goal of making money or selling the underlying asset at a greater price in the future.

Any asset or instrument bought with the goal that it would immediately generate income (such dividends or rental income) or with the aim of selling it for more than the original purchase price at a later date (capital gains) is considered a financial investment.

An Investment: What Is It?

The precise standards under which a transaction qualifies as an investment, however, are less clear. Generally speaking, there are a plethora of distinct investing categories.

various transactions may be considered investments by various persons, particularly when it comes to accounting. For instance, some people would view a leasing deal as an investment, while others might not.

By definition, an investment might include any activity or operation that is carried out with the goal of producing revenue in the future. As a result, creating things with the goal of selling them later on can also be considered an investment.

Certain kinds of transactions are readily seen as investments in money. These are discussed below and serve as the article’s main topic.

Which Different Investment Methods Are There?

Three categories, or “investment methods,” may be used to simply classify investments. These are as follows:

- Loan investments under debt

- Investments in equity (ownership of the firm)

- investments that are hybrid (preferred shares, mezzanine capital, convertible securities)

Debt Investing

Two more subcategories of debt-based investments are public and non-public (private) investments.

Any investment that may be bought or sold on open debt markets is considered a public debt investment. These include, among other things, bonds, debentures, and credit swaps. Public securities are frequently categorized by a corporation as held-to-maturity, held-for-trading, or available-for-sale. Accounting standards specify criteria and practices for each of these groupings.

Any transactions that result in an asset on the balance sheet but are not readily or publicly sold in marketplaces are considered private debt investments. Purchasing a different company’s loan or accounts receivable, which are anticipated to provide income in the future, is one example.

Investments in Equity

Public and non-public investments are additional categories for equity investments. The latter is more widely referred to as private equity, and it’s seen as a high-risk, high-reward venture. Although they have the potential to yield larger profits, equity investments are actually often seen as riskier than debt ones.

Any equity-based investment that is available for purchase or trading on a market is considered a public equity investment. When someone talks about investing, these are frequently the kinds of investments that come to mind. This includes securities like warrants, options, and ordinary and preferred shares.

Larger-scale investments, such as those in private equity, are frequently outside the purview of small investors. Among the most popular forms of private equity transactions are venture capital investments, mergers and acquisitions, and leveraged buyouts.

Investment Strategies that are Hybrid

Let’s examine a few more investing strategies. Certain investing strategies combine aspects of debt and equity. Mezzanine debt is one instance of this, when an investor lends money to another entity in return for stock. An additional illustration would be a convertible bond, when an investor buys a bond with the ability to swap it for a specific quantity of the issuing company’s stock shares.

Additionally, there are investment kinds that don’t include any elements of debt or equity. Any investment made on the asset side of the balance sheet, such buying machinery or real estate under PP&E, is an example of this kind. Alternatively, depending on the approach, buying intangible assets like a patent or trademark may also be considered an investment.

Last but not least, a sizable category of assets known as derivatives is derived from other securities, as the name suggests. There are several varieties of derivatives, each deserving of its own article. Nonetheless, futures and options, which are financial instruments whose values are based on an underlying stock or commodity, are instances of well-known derivatives.

How Does Valuation Work?

The process of ascertaining the current worth of a business, investment, or asset is referred to as valuation. Several widely used methods of valuation are listed below. When attempting to assign a value to an asset, analysts typically consider the potential earnings that the asset or firm may provide in the future.

On the other hand, the idea of intrinsic value describes a security’s perceived value based on potential profits or other characteristics unrelated to its market value. Thus, the task of analysts doing a valuation is to determine if the market has overvalued or undervalued a firm or an investment.

Motives for Conducting an Assessment

Since valuation may be used to find mispriced securities or suggest initiatives in which a corporation should invest, it is a crucial activity. Below is a list of some of the primary justifications for doing a valuation.

Purchase or Sale of a Business

The worth of a firm will often change between buyers and sellers. A valuation would be helpful to both parties when deciding whether to purchase or sell, and at what price.

Methodical organizing

Investments in initiatives that raise a company’s net present value should only be made. As a result, every investment choice is really a mini-evaluation predicated on the possibility of future wealth generation and profitability.

Funding for capital

When negotiating with banks or any other possible investors for finance, an objective appraisal could be helpful. Providing proof of a business’s value and cash flow generation capabilities makes it more credible to equity investors and lenders.

Investing in securities

Purchasing a security, such a stock or bond, is simply a wager that the asset’s market value isn’t being accurately reflected. Determining that inherent worth requires a valuation.

Company Valuation Approaches

Industry practitioners utilize three primary valuation methodologies when assessing a firm as a continuing concern:

(1) DCF analysis,

(2) similar company analysis, and

(3) precedent transactions.

These are the most often utilized techniques for valuation in the majority of finance-related fields, including corporate growth, investment banking, equity research, private equity, mergers and acquisitions (M&A), and leveraged buyouts (LBO).

There are three methods one might employ when valuing a business or asset, as the following picture illustrates. The asset method determines each asset’s fair market value, frequently factoring in the cost of construction or replacement.

When evaluating real estate, including commercial, new construction, and special-use buildings, the asset approach technique might be helpful.

The income technique comes next, and the most used method is the discounted cash flow (DCF). The most comprehensive and in-depth method of value modelling is a DCF.

The market method, a type of relative valuation that is often employed in the financial sector, is the last strategy. Analyses of similar companies and historical transactions are included.

First method: DCF analysis

Using the weighted average cost of capital (WACC) of the company, an analyst projects the unlevered free cash flow of a corporation into the future and discounts it back to the present in discounted cash flow (DCF) analysis, an intrinsic value method.

Making an Excel financial model is the first step in performing a DCF analysis, which requires extensive investigation and research. Of the three methods, this one is the most in-depth and necessitates the greatest guesswork and estimation.

Because there are so many inputs involved in creating a DCF model, the work necessary to prepare one may frequently provide the least accurate assessment. On the other hand, an analyst may anticipate value using a DCF model and even do a sensitivity analysis depending on several scenarios.

In the case of bigger enterprises, the DCF value is often calculated by a sum-of-the-parts approach, in which distinct business units are separately modelled and aggregated.

Method 2: examination of comparable companies, or “comps”

Comparable company analysis, sometimes known as “trading comps,” is a relative valuation approach that compares the present value of a company to other similar firms by examining trade multiples like P/E, EV/EBITDA, or other multiples.

The “comps” valuation method generates an observable value for the firm based on the existing values of other similar enterprises. Comps are the most often used approach since the multiples are easy to calculate and are always current.

According to this reasoning, firm Y’s stock must be worth $25.00 per share if it has earnings of $2.50 per share and company X trades at a 10-times P/E ratio (assuming the companies have identical risk and return characteristics).

Method 3: Transactions from the past

Another method of relative valuation is precedent transactions analysis, in which the firm under consideration is contrasted with other companies that have recently been purchased or sold in the same sector. The take-over premium that was factored into the acquisition price is reflected in these transaction figures.

The figures are a company’s whole worth, not simply a portion of it. They are helpful in M&A deals, but over time they can quickly become antiquated and no longer accurately represent the state of the market.

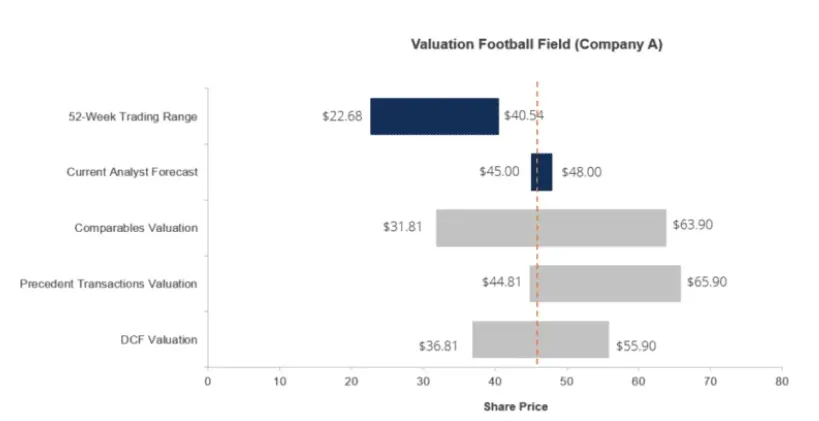

Football pitch map (condensed)

A football pitch chart is a common tool used by investment bankers to illustrate the range of valuations for a company based on several techniques of valuation. An illustration of a football pitch graph, which is commonly found in investment banking pitch books, is shown below.

As you can see, the graph displays the 52-week trading range of the company its stock price, if it is publicly traded), the range of prices that equity research analysts have determined for the stock,

the range of values derived from comparable valuation modelling, the range derived from prior transaction analysis, and lastly the DCF valuation method. The average valuation from all the approaches is shown by the orange dotted line in the Centre.

Additional techniques of appraisal

The ability-to-pay analysis is another technique used for valuing a going business. This method examines the highest price that an acquirer may pay for a company and yet meet a certain threshold.

What is the highest amount a private equity firm may pay for a business, for instance, if it has to reach a 30% hurdle rate?

If the business closes down, an estimated liquidation value will be determined by dismantling and liquidating the business’s assets. Since it is assumed that the assets will be sold as soon as possible to any buyer, this value is often greatly reduced.

Conclusion:

Check out our content to learn about valuation investing methods. Here we have detailed discussion on business investment. Hope you can get to know the investment methods well from here. If you want to get more content like this, you can know better about new business finance and investment from our homepage. Don’t forget to visit regularly to get more content like this. Also don’t forget to share our web address with your friends.